.jpg)

In 2025, Private equity seemed to be gradually reopening:

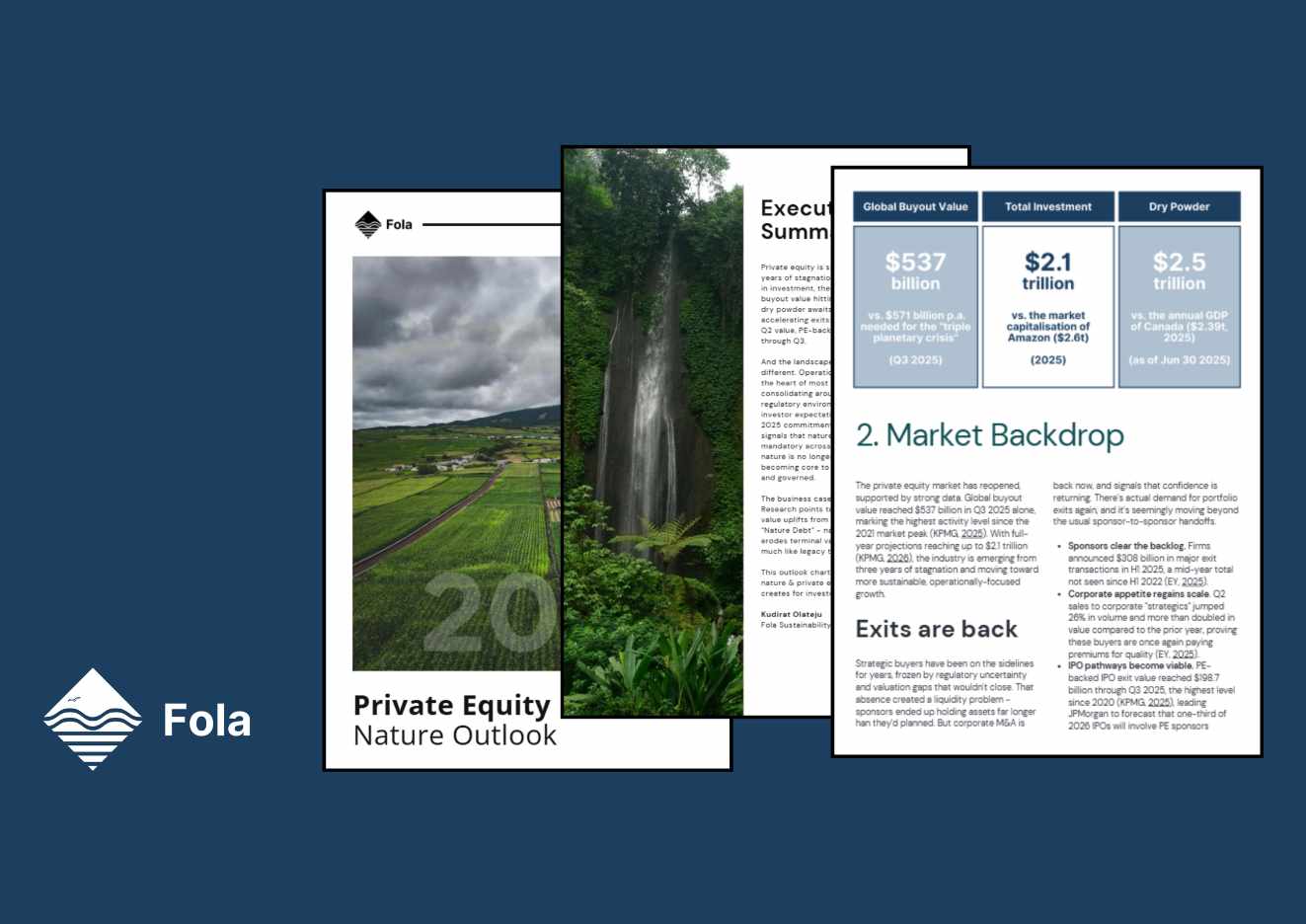

1. Global buyout value reached around USD 537 billion in Q3 2025

2. Full‑year private equity investment was estimated at USD 2.1 trillion - the strongest year since 2021

3. Dry powder remains above USD 2.5 trillion globally

4. Exit sentiment improved with multi-year highs seen in major exit transaction and PE-backed IPO exits

However, this rebound comes with a shift in priorities. While momentum is on the rise, fund managers are moving away from old strategies. Instead, they are focusing on operational value & real assets to navigate new pressures from regulation, litigation, and climate change.

The underlying realisation is simple: business stability cannot be financially engineered in tougher operating contexts - especially in the face of increasing physical and geopolitical shocks. Nature has long been one of the biggest, silent, providers of business stability, and the management of nature-related issues is rapidly becoming one of the biggest differentiators of success for businesses, investors and GPs globally.

This outlook report looks at private equity’s 2025 - 26 reset through a nature lens. It tracks how market dynamics and regulation are converging, and how nature can be a partner for value creation, or a quiet source of value destruction.

What’s inside the report

- Market backdrop: How the rebound in deals and exits is changing return drivers, and why operational value creation now dominates multiple expansion.

- Regulatory “winds”: What ISSB, CSRD, SEC climate rules and regional standards mean in practice for mid‑market and large-cap funds, and how far you really need to go on nature today.

- Nature as a value lever: Concrete examples from nature‑intensive sectors - agri‑food, logistics, consumer, forestry - where nature‑aligned operations are lifting EBITDA and resilience, not just “ticking ESG boxes”.

- The GP playbook: How to integrate nature into due diligence, portfolio value‑creation plans, management incentives and exit narratives in a way that investment committees can underwrite.

- Our take: “Nature debt”: Why unmanaged nature exposure is quietly building up as a form of hidden liability that will be priced in at exit.

Read the full report to see how leading GPs are moving from generic ESG language to nature‑aware value creation, and where the next wave of performance and downside protection is likely to come from.